{kind=link}

Giselleflissak/E+ through Getty Photos

Journey + Leisure (NYSE:TNL) has been quietly rebuilding its trip possession enterprise following the COVID pandemic. The corporate spun out of the worldwide hotelier big Wyndham, leaving many to query the corporate’s future, some even going so far as to recommend that the spin-out would sign the tip of the timeshare trade as we knew it. Issues have turned out fairly in a different way for the corporate. Underneath the management of trade veteran Michael Brown, the corporate has managed to face up to main structural modifications and a worldwide well being disaster that disproportionately affected the hospitality trade. As if that weren’t sufficient, the corporate is now going through the prospect of a serious world slowdown as central banks attempt to handle rampant inflation. Regardless of this, the corporate seems to be to be firing on all cylinders and is moving into an important subsequent few quarters that may present buyers with perception into the corporate’s resilience as we glance to begin the subsequent enterprise cycle.

Immediately we’ll check out Journey + Leisure and focus on what buyers can count on from the corporate going ahead (I’ve lined the corporate prior to now, for a extra detailed firm profile, try this text).

Firm Outlook

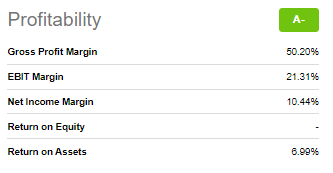

Following the spinout, I need to confess that I had my fair proportion of reservations as as to if the corporate may keep its sturdy gross sales quantity with out making concessions within the per-unit worth, which might, after all, affect gross margins. To this point, this concern has confirmed to be unfounded, as the corporate is posting gross revenue margins north of 60%.

In search of Alpha

That is a tremendous quantity. Keep in mind, this isn’t a software-as-a-service sort enterprise. As a substitute, the corporate is promoting trip possession pursuits in its current portfolio to clients it probably needed to pay advertising and marketing prices to accumulate. These advertising and marketing prices manifest primarily within the type of the items the corporate gives to entice folks into attending gross sales shows. Timeshares are notoriously powerful gross sales, and it usually takes a number of visits to lastly persuade a buyer to buy. This is the reason buyers are inclined to pay eager consideration to gross margin and advertising and marketing prices figures, because it gives main perception into the general attraction of the product. Proper now, Journey + Leisure is clearly knocking it out of the park.

Within the latest earnings name, the corporate reported a formidable Adjusted EBITDA of $230 million, which was good for an EPS of $1.27 cents. In addition they managed to provide a file quantity per visitor of $3489. Quantity per visitor is in impact the sum of money the corporate makes per tour it undertakes. The fascinating factor about that is that for the second quarter, greater than 65% of recent proprietor gross sales have been to Gen-Xers and millennials. The significance of this can’t be overstated when you think about the background of the timeshare trade. Airbnb (ABNB) and different various trip choices have been being touted as timeshare killers. The overall expectation was that as these companies turned extra fashionable, the timeshare trade would finally die out. The corporate managing to create worthwhile relationships with youthful house owners is so essential. It’s also value mentioning that new proprietor gross sales sometimes carry a decrease VPG than current proprietor gross sales, and that new house owners have a tendency to return again and buy extra possession down the road. The corporate additionally talked about that almost 80% of its proprietor base is touring debt free. This implies their trip possession is absolutely paid for, and their solely commitments are the annual upkeep charges. It will be truthful to say that the corporate it is at the moment in a superb place with its proprietor combine and is displaying indicators that it’s creating additional in the fitting course. However with the financial slowdown on the horizon, there are some issues concerning the enterprise mannequin’s vulnerability to defaults.

Debt Considerations

Timeshares are, at the start, a luxurious buy. Holidays are sometimes seen as non-obligatory endeavors, although they in all probability ought to take greater precedence. Timeshare corporations assist their clients go on trip by having them decide to the acquisition of an possession curiosity in a property or portfolio, permitting them to lock within the worth of their holidays for essentially the most half, other than occasional changes to annual upkeep charges. As a result of timeshares are usually expensive big-ticket purchases, clients are inclined to finance the acquisition not less than partly with debt. This observe is generally positive, and the corporate does an incredible job at screening its shoppers to guarantee that they’ll deal with the monetary commitments that come together with the acquisition. But when there have been to be a widespread financial slowdown because of the Federal Reserve tightening to deal with inflation, for instance, the fallout wouldn’t solely dent shopper confidence which might be a headwind for brand new purchases, however it may additionally end in larger than regular delinquencies in financed trip possession merchandise which might turn into fairly problematic for a lot of these corporations. The great factor is that these corporations have gotten higher at working with clients by tough instances to maintain their house owners pleased and to stop widespread injury to the corporate.

Valuation And Ahead-Trying Commentary

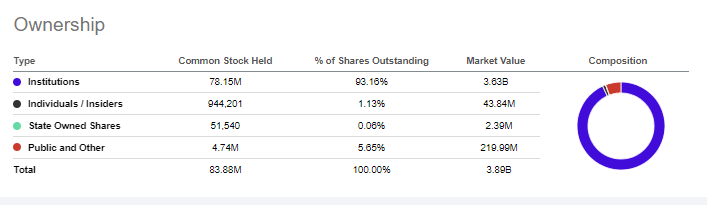

Regardless of these issues, Journey + Leisure nonetheless attracts a number of the premier buyers on the planet. Establishments personal a whopping 93% of shares excellent, which is at all times an incredible signal each time there are issues a few recession.

In search of Alpha

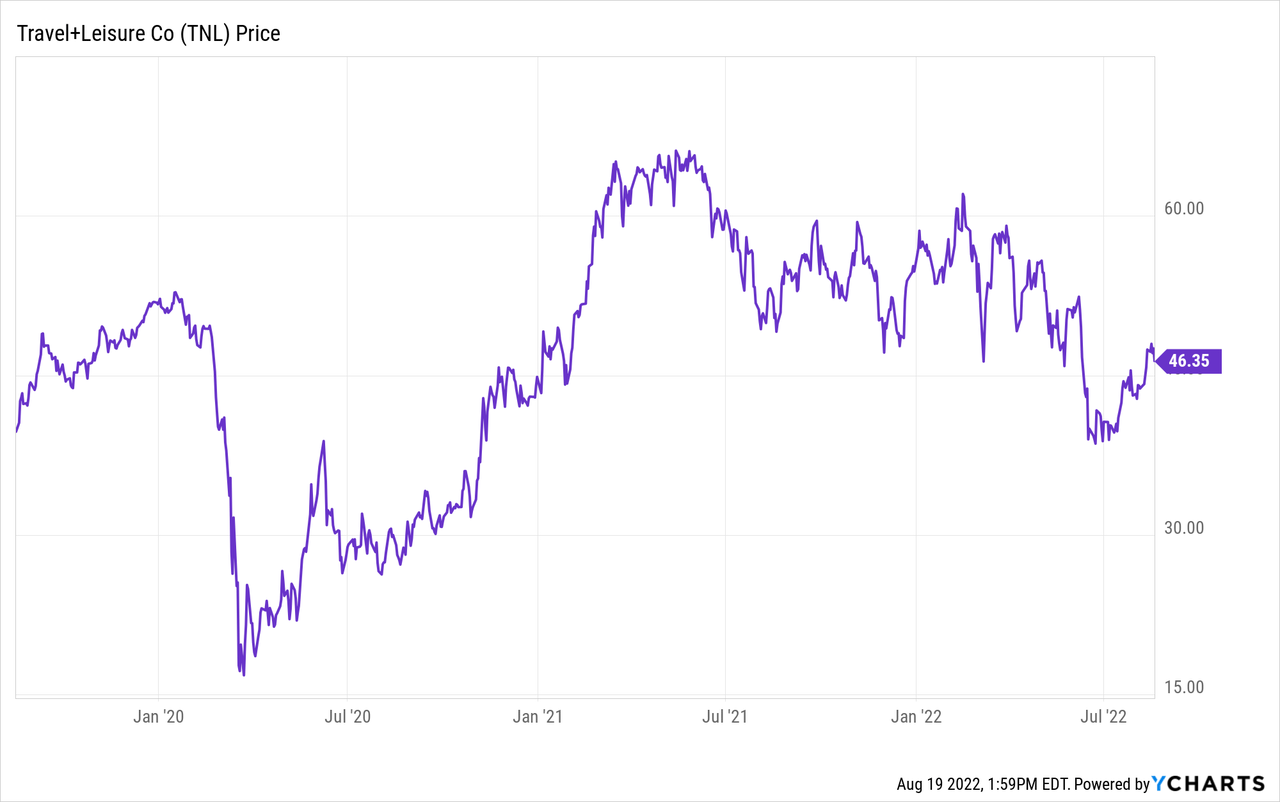

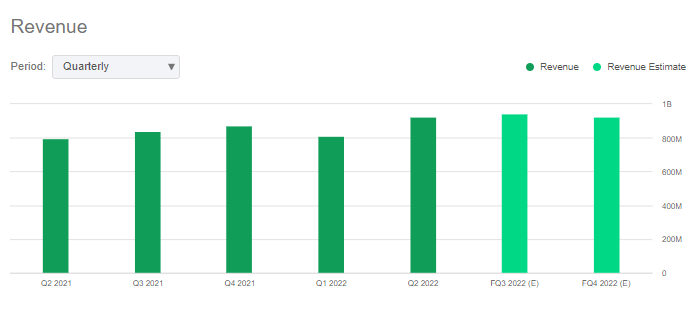

The corporate can be in the midst of a strong restoration from the COVID-19 pandemic, and regardless of the seasonal nature of income within the hospitality trade, income traits have been roughly steady, which is an efficient signal.

In search of Alpha

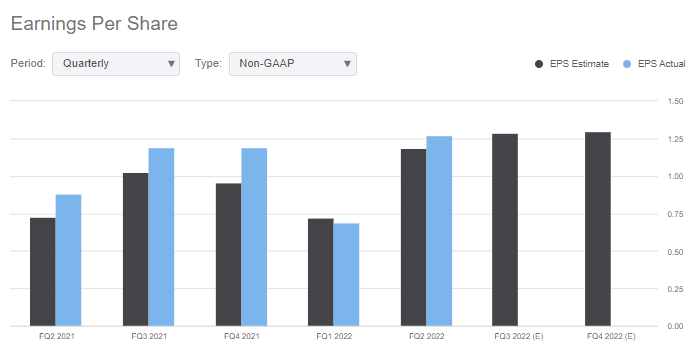

The administration crew has had a strong observe file of delivering to earnings expectations, and we are able to see that for the final 5 quarters, they’ve carried out exceptionally properly with 4 beats and one small miss. It’s also value mentioning that the winter interval tends to be one of many stronger quarters for timeshare corporations.

In search of Alpha

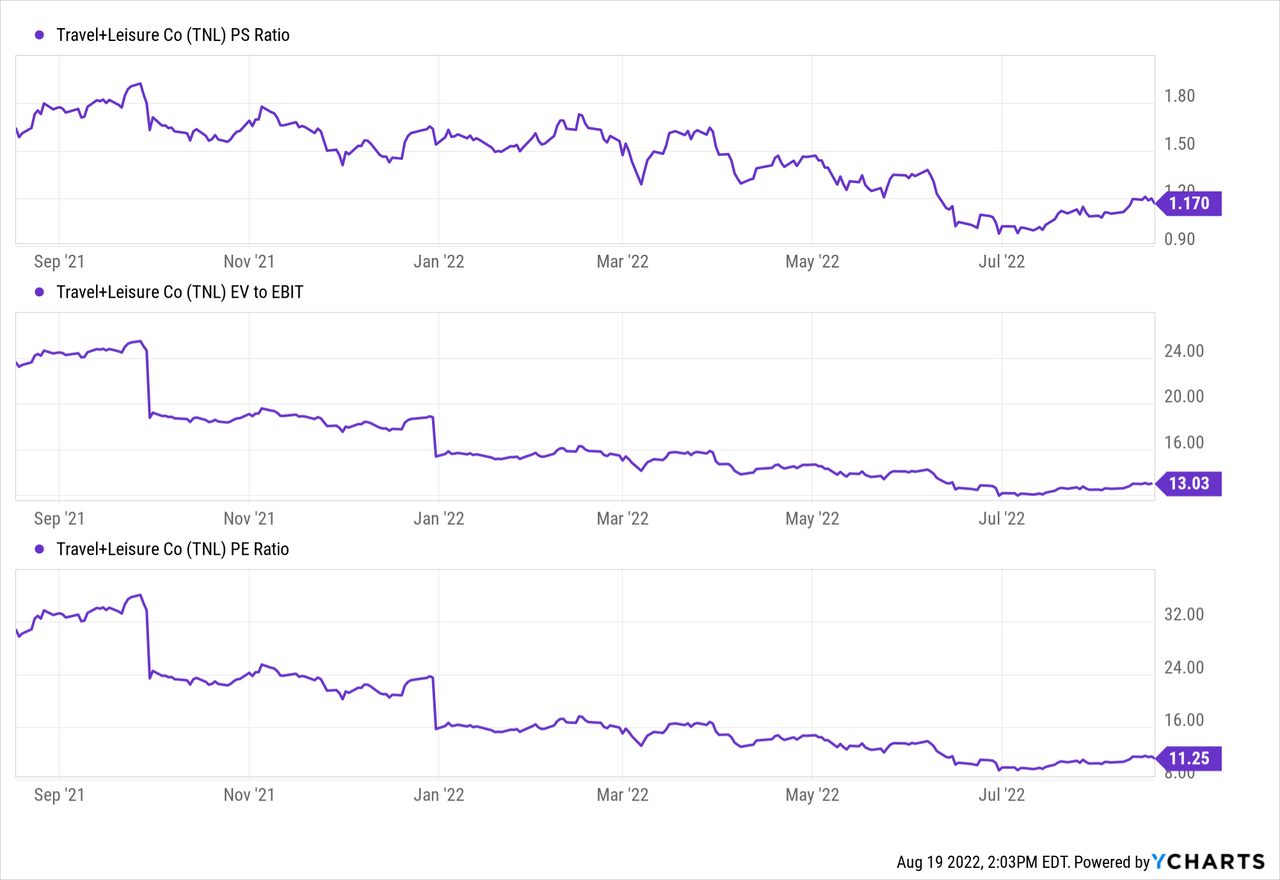

The corporate can be buying and selling on the low finish of its historic ranges for many of the essential multiples, which normally implies worth.

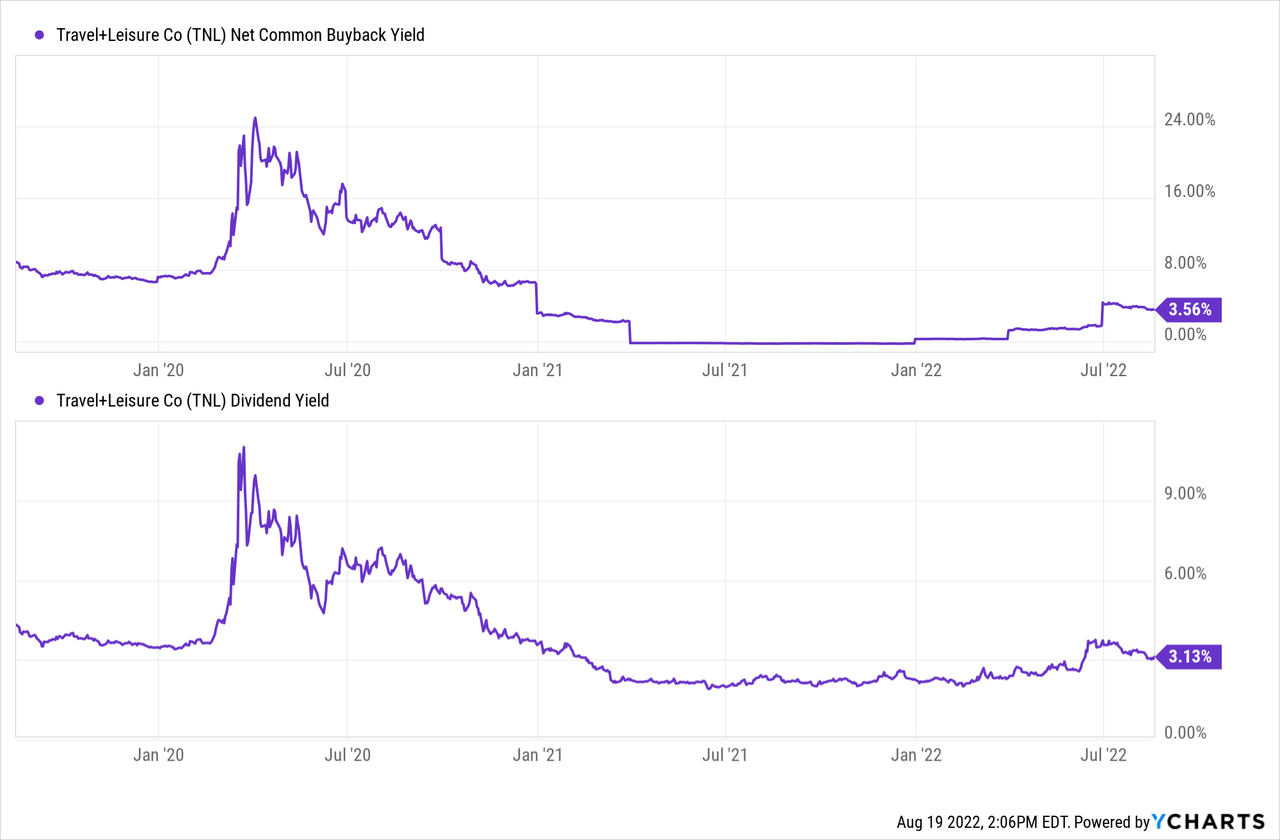

There’s additionally the strong dividend and good observe file of repurchases on this house that may present some incentive for buyers whereas they look forward to the commerce to pan out.

The Takeaway

In closing, the principle spotlight right here is the advance within the penetration of the youthful phase of the financial system. The danger of defaults is, after all, heightened in the intervening time, however a reasonably excessive proportion of the corporate’s house owners have paid off their loans. In the long run, I do imagine that Journey + Leisure shall be greater than present ranges, however within the brief time period, there are some severe dangers for the investor to contemplate earlier than taking a place. Because of this, I price Journey + Leisure a long-term purchase.